| front |1 |2 |3 |4 |5 |6 |7 |8 |9 |10 |11 |12 |13 |14 |15 |16 |17 |18 |19 |20 |21 |22 |23 |24 | 25|26 |27 |28 |29 |30 |31 |32 |33 |34 |35 |36 |37 |38 |39 |40 |41 |42 |43 |44 |45 |46 |47 |48 |49 |50 |51 |52 |53 |54 |review |

|

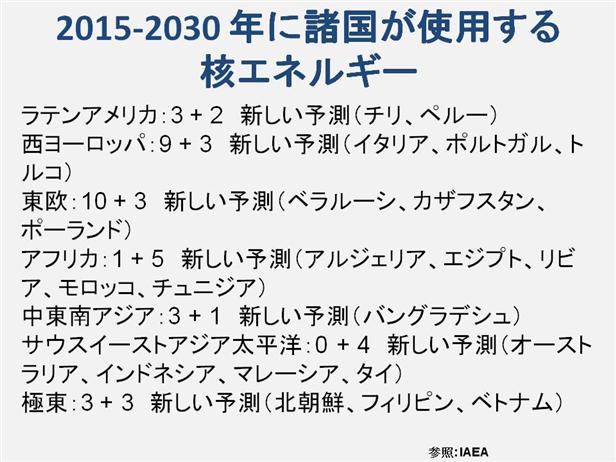

ラテンアメリカ:3

+ 2 新しい予測(チリ、ペルー)

Future of the industry In total about 21 new countries are considering to start using nuclear energy during 2015-2030 Diablo Canyon Power Plant in San Luis Obispo County, California, USA As of 2007, Watts Bar 1, which came on-line in February 7, 1996, was the last U.S. commercial nuclear reactor to go on-line. This is often quoted as evidence of a successful worldwide campaign for nuclear power phase-out. However, even in the U.S. and throughout Europe, investment in research and in the nuclear fuel cycle has continued, and some nuclear industry experts predict electricity shortages, fossil fuel price increases, global warming and heavy metal emissions from fossil fuel use, new technology such as passively safe plants, and national energy security will renew the demand for nuclear power plants. According to the World Nuclear Association, globally during the 1980s one new nuclear reactor started up every 17 days on average, and by the year 2015 this rate could increase to one every 5 days. Many countries remain active in developing nuclear power, including China, India, Japan and Pakistan. all actively developing both fast and thermal technology, South Korea and the United States, developing thermal technology only, and South Africa and China, developing versions of the Pebble Bed Modular Reactor (PBMR). Several EU member states actively pursue nuclear programs, while some other member states continue to have a ban for the nuclear energy use. Japan has an active nuclear construction program with new units brought on-line in 2005. In the U.S., three consortia responded in 2004 to the U.S. Department of Energy's solicitation under the Nuclear Power 2010 Program and were awarded matching funds�the Energy Policy Act of 2005 authorized loan guarantees for up to six new reactors, and authorized the Department of Energy to build a reactor based on the Generation IV Very-High-Temperature Reactor concept to produce both electricity and hydrogen. As of the early 21st century, nuclear power is of particular interest to both China and India to serve their rapidly growing economies�both are developing fast breeder reactors. (See also energy development). In the energy policy of the United Kingdom it is recognized that there is a likely future energy supply shortfall, which may have to be filled by either new nuclear plant construction or maintaining existing plants beyond their programmed lifetime. There is a possible impediment to production of nuclear power plants as only a few companies worldwide have the capacity to forge single-piece reactor pressure vessels, which are necessary in most reactor designs. Utilities across the world are submitting orders years in advance of any actual need for these vessels. Other manufacturers are examining various options, including making the component themselves, or finding ways to make a similar item using alternate methods. Other solutions include using designs that do not require single-piece forged pressure vessels such as Canada's Advanced CANDU Reactors or Sodium-cooled Fast Reactors. This graph illustrates the potential rise in CO2emissions if base-load electricity currently produced in the U.S. by nuclear power were replaced by coal or natural gas as current reactors go offline after their 60 year licenses expire. Note: graph assumes all 104 American nuclear power plants receive license extensions out to 60 years. The World Nuclear Industry Status Report 2009 states that "even if Finland and France each builds a reactor or two, China goes for an additional 20 plants and Japan, Korea or Eastern Europe add a few units, the overall worldwide trend will most likely be downwards over the next two decades". With long lead times of 10 years or more, it will be difficult to maintain or increase the number of operating nuclear power plants over the next 20 years. The one exception to this outcome would be if operating lifetimes could be substantially increased beyond 40 years on average. This seems unlikely since the present average age of the operating nuclear power plant fleet in the world is 25 years. However, China plans to build more than 100 plants, while in the US the licenses of almost half its reactors have already been extended to 60 years, and plans to build more than 30 new ones are under consideration. Further, the U.S. NRC and the U.S. Department of Energy have initiated research into Light water reactor sustainability which is hoped will lead to allowing extensions of reactor licenses beyond 60 years, in increments of 20 years, provided that safety can be maintained, as the loss in non-CO2-emitting generation capacity by retiring reactors "may serve to challenge U.S. energy security, potentially resulting in increased greenhouse gas emissions, and contributing to an imbalance between electric supply and demand." In 2008, the International Atomic Energy Agency (IAEA) predicted that nuclear power capacity could double by 2030, though that would not be enough to increase nuclear's share of electricity generation. |